.gif) |

| Ed Sullivan |

Several factors are creating uptick in economic activity in the U.S. in 2015. During C&D World, the annual meeting of the Construction & Demolition Recycling Association (CDRA), March 29-31, in Nashville, Tennessee, Ed Sullivan, chief economist of the Portland Cement Association (PCA), District of Columbia, shared the association’s predictions for the coming years. Sullivan, who noted he has a reputation for being a conservative construction economist said, “I am among the most optimistic economists in the construction industry today.”

He said PCA is seeing improvement in the cement and construction industries, job growth, consumer spending coming back, bottom lines of corporations improving and banks in the strongest positions they have been in recent years. A result of coming out of the recession, he said, is pent-up demand.

“You don’t need an economist to be optimistic, you see it in your day-to-day operations,” he said. “It’s a different game.”

Sullivan said construction activity pace will double from 2.5 percent to 5 percent. The 5 percent increase is expected to last into 2019. In the near-term most activity will be in residential, but nonresidential will also continue to improve, he said.

“This is the first time in eight years that you’ve had residential, nonresidential and public all contributing to growth. In my industry when that happens, it is not unusual to see double-digit growth rates,” said Sullivan.

He said lower oil prices are critical to stronger overall economic activity, and longer term it will pass through onto construction activity. Regions that depend on oil production, however, will be negatively affected.

PCA’s forecast looks at 26 different construction sectors and Sullivan said the oil and the improvement sectors are the only two where the association sees problems.

Declining unemployment will cause wage pressures to rise and put more money in people’s pockets, explained Sullivan. The double-dip recession caused pent-up demand.

“The recession has healed us and put us in a position to jump. We believe that consumers are ready to propel stronger economic growth,” he said.

He said he expects gross domestic product (GDP) growth to be around 3 percent, to 3.5 percent annually.

A curve ball occurred when oil prices dropped, noted Sullivan. He said the drop in prices benefit most areas of the economy with the exception of the energy sector and the drilling and construction activity related to it. He predicted a 32 percent drop in drilling and related construction. He noted that construction activity in other areas benefits from the stronger economic activity that results from lower oil prices, but it takes about one to two years to have an impact.

He said PCA is seeing improvement in the cement and construction industries, job growth, consumer spending coming back, bottom lines of corporations improving and banks in the strongest positions they have been in recent years. A result of coming out of the recession, he said, is pent-up demand.

“You don’t need an economist to be optimistic, you see it in your day-to-day operations,” he said. “It’s a different game.”

Sullivan said construction activity pace will double from 2.5 percent to 5 percent. The 5 percent increase is expected to last into 2019. In the near-term most activity will be in residential, but nonresidential will also continue to improve, he said.

“This is the first time in eight years that you’ve had residential, nonresidential and public all contributing to growth. In my industry when that happens, it is not unusual to see double-digit growth rates,” said Sullivan.

He said lower oil prices are critical to stronger overall economic activity, and longer term it will pass through onto construction activity. Regions that depend on oil production, however, will be negatively affected.

PCA’s forecast looks at 26 different construction sectors and Sullivan said the oil and the improvement sectors are the only two where the association sees problems.

Declining unemployment will cause wage pressures to rise and put more money in people’s pockets, explained Sullivan. The double-dip recession caused pent-up demand.

“The recession has healed us and put us in a position to jump. We believe that consumers are ready to propel stronger economic growth,” he said.

He said he expects gross domestic product (GDP) growth to be around 3 percent, to 3.5 percent annually.

A curve ball occurred when oil prices dropped, noted Sullivan. He said the drop in prices benefit most areas of the economy with the exception of the energy sector and the drilling and construction activity related to it. He predicted a 32 percent drop in drilling and related construction. He noted that construction activity in other areas benefits from the stronger economic activity that results from lower oil prices, but it takes about one to two years to have an impact.

Housing starts are expected to rise 17 percent in 2015, according to Sullivan, but he put that number in perspective by saying that it only amounts to about 1.1 million houses; when at its peak, housing starts were at 2.1 million.

“We are still nowhere near our past historical levels,” he said. Even at that same growth rate by 2019 growth is still only at 2002-2003 averages.

“I am an optimist, but I am by no means wild-eyed,” he added.

He also noted that mortgage-to-rent ratios are favorable in many areas and sales activity has increased by 6 percent. The housing boom and bust was greatest felt on the coasts and PCA predicts the coastal areas of the U.S. will reclaim some of that home values, but growth will be steadier.

“Right now we calculate 4.1 million units of pent-up housing demand,” Sullivan said.

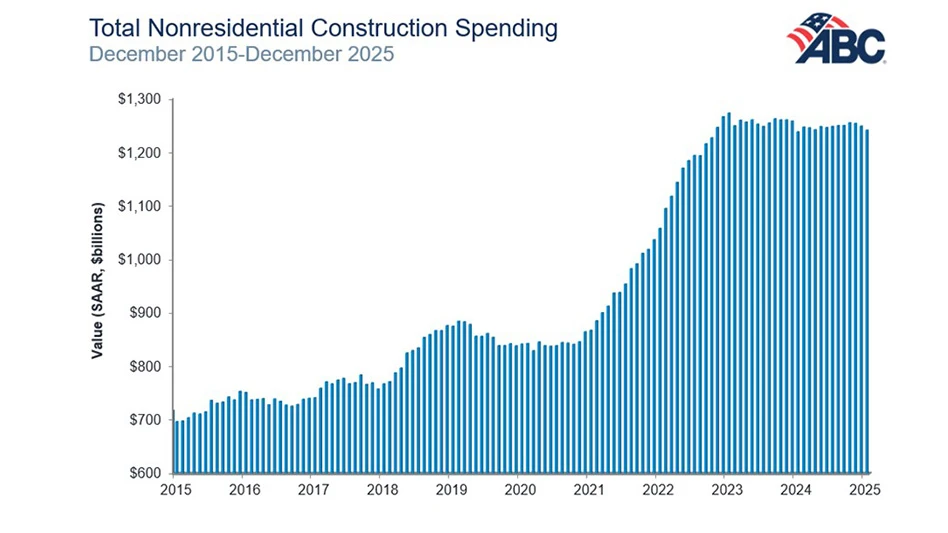

Nonresidential building is still not at past peak levels either, said Sullivan. During the recession, leasing rates crashed and vacancy rates increased, but that is changing. As about 600,000 new office workers have entered the workforce, vacancy rates have declined and are now at about 14.5 percent. As more jobs are created, vacancy rates in offices are declining and creating more operating income for property owners as well as asset appreciation.

“Some version of this is happening in every nonresidential sector, and it is being pushed through by jobs,” Sullivan said. He explained the U.S. needs 35 million office workers to achieve full occupancy and 30 million to create stable leasing rates. The current number office workers is 30.4 million.

“We are seeing growth in offices. It is occurring at different paces at different regions,” Sullivan said. “It is only going to continue to improve because this cycle hasn’t finished yet, and it will continue as long as you have jobs growth.”

Of all nonresidential sectors, only hospitals and institutions, religious and education showed a decline in growth in 2014. In 2015, only the hospitals and institutions segment is expected to see a decline of approximately 1.8 percent while all other areas will experience some growth. By 2016, growth is expected in all categories.

Public sector construction will improve despite gridlock in the District of Columbia also due to public pent-up demand, according to Sullivan. More spending on transportation and other construction projects is expected from the state level. He explained that during the recession, state budgets were cut due to less tax revenue, projects were prioritized and taxes were raised. This created public pent-up demand, and after seven years of decline, the PCA is predicting a 1.6 percent growth in 2015 “as state finances continue to improve,” Sullivan said. Home prices have been rising three years in a row, further suggesting local government construction activity also will increase this year, he added.

“We are optimistic,” said Sullivan, who noted that each segment’s growth could be stronger and faster when population growth is factored in. The population in the U.S. is expected to grow by 42 million persons by 2030 who will need police stations, schools and hospitals, he said.

The PCA will release its spring 2015 forecast April 8.

C&D World was held March 29-30 at the Music City Center in Nashville.

“We are still nowhere near our past historical levels,” he said. Even at that same growth rate by 2019 growth is still only at 2002-2003 averages.

“I am an optimist, but I am by no means wild-eyed,” he added.

He also noted that mortgage-to-rent ratios are favorable in many areas and sales activity has increased by 6 percent. The housing boom and bust was greatest felt on the coasts and PCA predicts the coastal areas of the U.S. will reclaim some of that home values, but growth will be steadier.

“Right now we calculate 4.1 million units of pent-up housing demand,” Sullivan said.

Nonresidential building is still not at past peak levels either, said Sullivan. During the recession, leasing rates crashed and vacancy rates increased, but that is changing. As about 600,000 new office workers have entered the workforce, vacancy rates have declined and are now at about 14.5 percent. As more jobs are created, vacancy rates in offices are declining and creating more operating income for property owners as well as asset appreciation.

“Some version of this is happening in every nonresidential sector, and it is being pushed through by jobs,” Sullivan said. He explained the U.S. needs 35 million office workers to achieve full occupancy and 30 million to create stable leasing rates. The current number office workers is 30.4 million.

“We are seeing growth in offices. It is occurring at different paces at different regions,” Sullivan said. “It is only going to continue to improve because this cycle hasn’t finished yet, and it will continue as long as you have jobs growth.”

Of all nonresidential sectors, only hospitals and institutions, religious and education showed a decline in growth in 2014. In 2015, only the hospitals and institutions segment is expected to see a decline of approximately 1.8 percent while all other areas will experience some growth. By 2016, growth is expected in all categories.

Public sector construction will improve despite gridlock in the District of Columbia also due to public pent-up demand, according to Sullivan. More spending on transportation and other construction projects is expected from the state level. He explained that during the recession, state budgets were cut due to less tax revenue, projects were prioritized and taxes were raised. This created public pent-up demand, and after seven years of decline, the PCA is predicting a 1.6 percent growth in 2015 “as state finances continue to improve,” Sullivan said. Home prices have been rising three years in a row, further suggesting local government construction activity also will increase this year, he added.

“We are optimistic,” said Sullivan, who noted that each segment’s growth could be stronger and faster when population growth is factored in. The population in the U.S. is expected to grow by 42 million persons by 2030 who will need police stations, schools and hospitals, he said.

The PCA will release its spring 2015 forecast April 8.

C&D World was held March 29-30 at the Music City Center in Nashville.

Latest from Construction & Demolition Recycling

- Vecoplan to present modular solutions at IFAT 2026

- Terex Ecotec appoints Bradley Equipment as Texas distributor

- Greenwave raises revenue but loses money in Q2 2025

- Recycled steel prices hold steady

- John Deere launches ‘Building America’ excavator contest

- Triumvirate Environmental acquires Environmental Waste Minimization

- Coastal Waste & Recycling expands recycling operations with Machinex

- Reconomy acquires German-based GfAW